Spring Hotels' acquisition and near-doubling of its property portfolio following the Mare Nostrum purchase marks a critical inflection in how mid-market European operators are now competing through rapid asset consolidation rather than organic development. Unlike last week's signal (international luxury brands treating secondary Asian markets as destination anchors), this week's movement reveals that European operators face inverse pressure: they must achieve scale in their home markets to defend against both international brand encroachment and the fragmentation of independent inventory across multiple ownership structures. The Spanish operator's inventory expansion—achieved in twelve months rather than the typical 3–5 year development cycle—indicates that acquisition-driven consolidation is now the primary capital deployment mechanism for operators seeking to achieve distribution density and operational leverage before larger chains (Marriott, IHG, Hyatt) complete their own Mediterranean fill-in strategies. For hotel investors, this signals that standalone properties and small chains in Spain, Portugal, and Greece now face a narrowing window to either consolidate upward into larger platforms or accept permanent disadvantage in digital distribution, revenue management sophistication, and brand partnership economics. The coming months will reward operators who recognize that scale in mature European markets is no longer optional—it is the prerequisite for accessing modern capital, talent, and technology infrastructure.

Thai AirAsia's exploration of regional flight routes to Hua Hin, executed in partnership with Thailand's Tourism Authority, signals that low-cost carriers are now treating secondary city connectivity as a structural response to primary gateway saturation rather than a supplementary growth vector. Unlike last week's LATAM signal (loyalty networks creating recurring revenue independent of seat yield), this week's development reveals that Asian LCCs face an inverse constraint: they must expand beyond Bangkok and Phuket because those airports now operate at or near capacity utilization, forcing carriers to either cannibalize existing routes or develop new city pairs that bypass congested hubs. Thai AirAsia's Hua Hin strategy matters because it creates a direct feeder system to beach resorts and secondary destination hotels that have historically depended on ground transportation from Bangkok—a friction point that reduced frequency and increased customer acquisition costs for hospitality properties in regional markets. By establishing direct air access to Hua Hin, the carrier simultaneously reduces hotel booking friction, lowers the effective price of regional stays (by eliminating 2–3 hours of ground transfer), and creates a new distribution channel for properties that previously competed only within the Bangkok-centric travel ecosystem. We expect the coming months to see competitive responses from AirAsia's rivals (Nok Air, Thai Lion) targeting alternative secondary gateways, which will accelerate the fragmentation of Thai tourism away from Bangkok and create new revenue opportunities for operators positioned in Phuket, Chiang Mai, and secondary beach destinations.

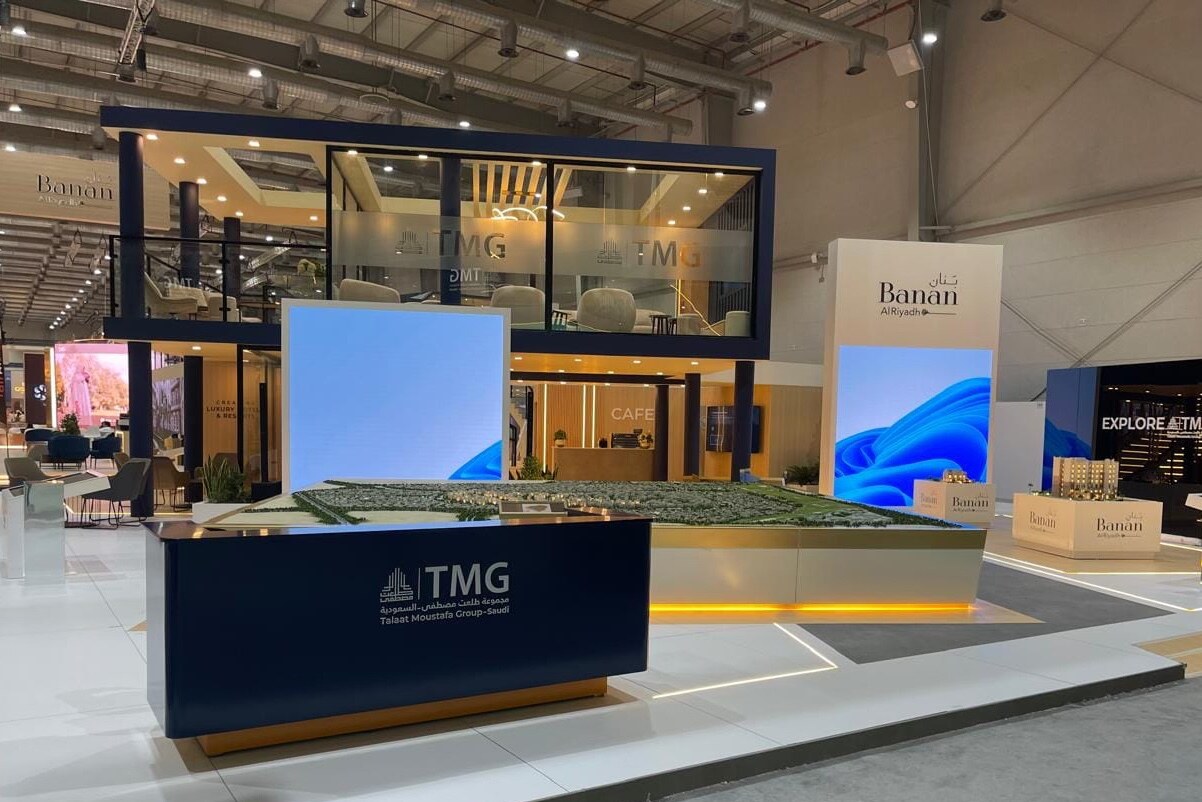

Talaat Moustafa Group's H1 2026 sales of $4.45 billion (up 3.8% year-over-year) demonstrate that Egyptian real estate developers are maintaining capital formation velocity despite macroeconomic headwinds, signaling sustained investor confidence in the country's hospitality-linked mixed-use development pipeline. Unlike last week's signal (Egypt's state IPO program creating transparent market-based capital formation), TMG's performance reveals that private developers are matching government-driven monetization with their own record sales velocity, creating a dual-track capital formation system where both state and private actors are simultaneously deploying capital into hospitality real estate. TMG's second-quarter performance—described as a record—indicates that the developer is maintaining pricing power and sales velocity even as interest rates remain elevated and regional geopolitical risks persist, suggesting that international and regional capital is now treating Egyptian hospitality-linked real estate as a structural allocation category rather than a cyclical opportunity. For hospitality operators and investors, TMG's sustained momentum matters because it signals that the Egyptian market now has sufficient capital formation infrastructure (both public and private) to support large-scale, multi-year hotel development programs without execution risk tied to financing gaps or developer insolvency. The coming months will test whether TMG's sales velocity persists through the second half of 2026, which will determine whether Egypt's hospitality expansion is driven by genuine demand or by front-loading of sales ahead of potential macroeconomic deterioration; operators should monitor TMG's Q3 and Q4 guidance closely as a leading indicator of capital formation sustainability.

Croatia's emphasis on lesser-known island destinations—combining ancient villages, dramatic landscapes, and crystal-clear seas—signals that luxury operators and travel platforms are now actively repositioning secondary Mediterranean geographies as primary alternatives to saturated coastal markets in Spain, Greece, and southern Italy. This positioning differs from last week's Minor Hotels signal (wellness as a standalone profit center) by revealing that destination-level brand building is now a primary competitive lever for regions seeking to capture affluent travelers who perceive mainstream Mediterranean destinations as commoditized. Croatian islands offer a distinct value proposition: they combine Mediterranean authenticity with lower visitor density than Santorini or the Amalfi Coast, creating a premium positioning that justifies luxury pricing without requiring the operational complexity of ultra-luxury resort development. For luxury operators and hospitality investors, Croatia's emergence matters because it creates a new portfolio anchor geography where operators can develop 150–300 room properties at luxury price points ($400–600 nightly rates) without competing directly against established five-star chains in saturated markets. The coming months will determine whether this repositioning gains traction among affluent travelers aged 45–65 (the primary demographic for Mediterranean luxury), which will either validate Croatian islands as a structural growth market or reveal that the positioning remains a niche play dependent on travel media amplification rather than genuine customer demand.

The AI Hospitality Alliance's 2026 member survey demonstrates that hospitality stakeholders are now shifting from abstract governance discussions toward pragmatic implementation guidance—indicating that the industry has moved beyond the pre-regulatory standard-setting phase and is now focused on operational deployment challenges. Unlike last week's signal (AIHA establishing self-regulatory frameworks before government mandates), this week's development reveals that operators face a different bottleneck: they understand the need for responsible AI but lack practical guidance on how to integrate AI systems into revenue management, labor scheduling, and customer service operations without creating execution risk or operational disruption. The survey data signals that operators are now asking implementation questions (How do we deploy AI without degrading customer experience? How do we train staff to work alongside AI systems? How do we manage data privacy in real-time revenue management?) rather than governance questions (What standards should we adopt? What compliance frameworks should we build?), indicating a maturation of the industry's AI adoption readiness. For technology vendors and hospitality operators, this shift matters because it creates a market opportunity for implementation-focused consulting, staff training programs, and AI-to-operations integration services that address the gap between AI capability and operational deployment. We expect the coming months to see AIHA pivot from standard-setting toward best-practice documentation and case studies that demonstrate how leading operators have successfully integrated AI into core revenue and operations functions, which will accelerate adoption across mid-market and smaller operators who currently lack in-house AI expertise.

The sixth edition of the Traveling for Happiness Awards signals that sustainability recognition programs are now functioning as a primary brand differentiation and market positioning tool for hospitality operators seeking to capture affluent, values-aligned travelers. Unlike last week's Iberostar signal (operators positioning themselves as primary actors in environmental governance through research partnerships), this week's development reveals that operators are translating environmental commitments into concrete, measurable operational changes that generate immediate brand value and customer loyalty benefits. The awards program's expansion and recognition across multiple editions indicates that hospitality operators now perceive sustainability not as a compliance cost or reputational hedge, but as a direct revenue lever that attracts higher-spending, lower-churn customer segments and justifies premium pricing. For hospitality investors and operators, the Traveling for Happiness framework matters because it provides a standardized, third-party validated sustainability positioning that allows mid-market and independent properties to compete against international chains on values-alignment without requiring the capital intensity of net-zero infrastructure investments. The coming months will likely see increased operator participation in sustainability award programs and accelerated integration of sustainability narratives into marketing and distribution strategies, which will create a competitive dynamic where non-participating operators face increasing perception disadvantage among affluent, environmentally conscious travelers—particularly in European and North American source markets where sustainability values drive booking decisions for 35–50% of luxury leisure travelers.

The convergence of three distinct regional movements—Spring Hotels' Mediterranean consolidation signaling that European operators must achieve scale through acquisition, Thai AirAsia's secondary gateway expansion fragmenting Asian tourism distribution away from primary hubs, and TMG's sustained sales velocity validating Egypt's dual-track capital formation system—creates fundamentally different competitive dynamics across three critical hospitality markets through the coming months and into 2027. European operators face a consolidation imperative: standalone and small-chain properties will face simultaneous pressure from acquisition-focused competitors, international brand expansion, and distribution disadvantage unless they achieve scale through M&A or strategic partnerships before the window for favorable acquisition multiples closes. Asian operators face a distribution opportunity: properties positioned in secondary gateways (Hua Hin, Chiang Mai, secondary Thai islands) will benefit from improved air connectivity and reduced customer acquisition friction, while Bangkok-centric operators will face margin compression as carriers fragment capacity away from primary hubs. Egyptian operators and investors face a capital formation advantage: the combination of private developer momentum (TMG) and public market infrastructure (state IPO programs) creates a rare window where hospitality-linked real estate can attract institutional capital at lower cost of capital than competing emerging markets, rewarding developers and operators who can deploy capital into large-scale, multi-year projects before regional competition intensifies. The regional winners through 2027 will be European consolidators who achieve critical mass before acquisition multiples compress, Asian secondary-market operators who can capture the first wave of gateway-fragmentation demand, and Egyptian developers who deploy capital before the capital formation window narrows—while losers will be fragmented European independents, primary-hub Asian operators facing capacity cannibalization, and Egyptian operators who delay capital deployment waiting for improved macroeconomic conditions that may not materialize.

Get the full market intelligence reports delivered weekly.

Market Intelligence

Spring Hotels' acquisition and near-doubling of its property portfolio following the Mare Nostrum purchase marks a critical inflection in how mid-market European operators are now competing through rapid asset consolidation rather than organic development. Unlike last week's signal (international luxury brands treating secondary Asian markets as destination anchors), this week's movement reveals that European operators face inverse pressure: they must achieve scale in their home markets to defend against both international brand encroachment and the fragmentation of independent inventory across multiple ownership structures. The Spanish operator's inventory expansion—achieved in twelve months rather than the typical 3–5 year development cycle—indicates that acquisition-driven consolidation is now the primary capital deployment mechanism for operators seeking to achieve distribution density and operational leverage before larger chains (Marriott, IHG, Hyatt) complete their own Mediterranean fill-in strategies. For hotel investors, this signals that standalone properties and small chains in Spain, Portugal, and Greece now face a narrowing window to either consolidate upward into larger platforms or accept permanent disadvantage in digital distribution, revenue management sophistication, and brand partnership economics. The coming months will reward operators who recognize that scale in mature European markets is no longer optional—it is the prerequisite for accessing modern capital, talent, and technology infrastructure.

Thai AirAsia's exploration of regional flight routes to Hua Hin, executed in partnership with Thailand's Tourism Authority, signals that low-cost carriers are now treating secondary city connectivity as a structural response to primary gateway saturation rather than a supplementary growth vector. Unlike last week's LATAM signal (loyalty networks creating recurring revenue independent of seat yield), this week's development reveals that Asian LCCs face an inverse constraint: they must expand beyond Bangkok and Phuket because those airports now operate at or near capacity utilization, forcing carriers to either cannibalize existing routes or develop new city pairs that bypass congested hubs. Thai AirAsia's Hua Hin strategy matters because it creates a direct feeder system to beach resorts and secondary destination hotels that have historically depended on ground transportation from Bangkok—a friction point that reduced frequency and increased customer acquisition costs for hospitality properties in regional markets. By establishing direct air access to Hua Hin, the carrier simultaneously reduces hotel booking friction, lowers the effective price of regional stays (by eliminating 2–3 hours of ground transfer), and creates a new distribution channel for properties that previously competed only within the Bangkok-centric travel ecosystem. We expect the coming months to see competitive responses from AirAsia's rivals (Nok Air, Thai Lion) targeting alternative secondary gateways, which will accelerate the fragmentation of Thai tourism away from Bangkok and create new revenue opportunities for operators positioned in Phuket, Chiang Mai, and secondary beach destinations.

Talaat Moustafa Group's H1 2026 sales of $4.45 billion (up 3.8% year-over-year) demonstrate that Egyptian real estate developers are maintaining capital formation velocity despite macroeconomic headwinds, signaling sustained investor confidence in the country's hospitality-linked mixed-use development pipeline. Unlike last week's signal (Egypt's state IPO program creating transparent market-based capital formation), TMG's performance reveals that private developers are matching government-driven monetization with their own record sales velocity, creating a dual-track capital formation system where both state and private actors are simultaneously deploying capital into hospitality real estate. TMG's second-quarter performance—described as a record—indicates that the developer is maintaining pricing power and sales velocity even as interest rates remain elevated and regional geopolitical risks persist, suggesting that international and regional capital is now treating Egyptian hospitality-linked real estate as a structural allocation category rather than a cyclical opportunity. For hospitality operators and investors, TMG's sustained momentum matters because it signals that the Egyptian market now has sufficient capital formation infrastructure (both public and private) to support large-scale, multi-year hotel development programs without execution risk tied to financing gaps or developer insolvency. The coming months will test whether TMG's sales velocity persists through the second half of 2026, which will determine whether Egypt's hospitality expansion is driven by genuine demand or by front-loading of sales ahead of potential macroeconomic deterioration; operators should monitor TMG's Q3 and Q4 guidance closely as a leading indicator of capital formation sustainability.

Croatia's emphasis on lesser-known island destinations—combining ancient villages, dramatic landscapes, and crystal-clear seas—signals that luxury operators and travel platforms are now actively repositioning secondary Mediterranean geographies as primary alternatives to saturated coastal markets in Spain, Greece, and southern Italy. This positioning differs from last week's Minor Hotels signal (wellness as a standalone profit center) by revealing that destination-level brand building is now a primary competitive lever for regions seeking to capture affluent travelers who perceive mainstream Mediterranean destinations as commoditized. Croatian islands offer a distinct value proposition: they combine Mediterranean authenticity with lower visitor density than Santorini or the Amalfi Coast, creating a premium positioning that justifies luxury pricing without requiring the operational complexity of ultra-luxury resort development. For luxury operators and hospitality investors, Croatia's emergence matters because it creates a new portfolio anchor geography where operators can develop 150–300 room properties at luxury price points ($400–600 nightly rates) without competing directly against established five-star chains in saturated markets. The coming months will determine whether this repositioning gains traction among affluent travelers aged 45–65 (the primary demographic for Mediterranean luxury), which will either validate Croatian islands as a structural growth market or reveal that the positioning remains a niche play dependent on travel media amplification rather than genuine customer demand.

The AI Hospitality Alliance's 2026 member survey demonstrates that hospitality stakeholders are now shifting from abstract governance discussions toward pragmatic implementation guidance—indicating that the industry has moved beyond the pre-regulatory standard-setting phase and is now focused on operational deployment challenges. Unlike last week's signal (AIHA establishing self-regulatory frameworks before government mandates), this week's development reveals that operators face a different bottleneck: they understand the need for responsible AI but lack practical guidance on how to integrate AI systems into revenue management, labor scheduling, and customer service operations without creating execution risk or operational disruption. The survey data signals that operators are now asking implementation questions (How do we deploy AI without degrading customer experience? How do we train staff to work alongside AI systems? How do we manage data privacy in real-time revenue management?) rather than governance questions (What standards should we adopt? What compliance frameworks should we build?), indicating a maturation of the industry's AI adoption readiness. For technology vendors and hospitality operators, this shift matters because it creates a market opportunity for implementation-focused consulting, staff training programs, and AI-to-operations integration services that address the gap between AI capability and operational deployment. We expect the coming months to see AIHA pivot from standard-setting toward best-practice documentation and case studies that demonstrate how leading operators have successfully integrated AI into core revenue and operations functions, which will accelerate adoption across mid-market and smaller operators who currently lack in-house AI expertise.

The sixth edition of the Traveling for Happiness Awards signals that sustainability recognition programs are now functioning as a primary brand differentiation and market positioning tool for hospitality operators seeking to capture affluent, values-aligned travelers. Unlike last week's Iberostar signal (operators positioning themselves as primary actors in environmental governance through research partnerships), this week's development reveals that operators are translating environmental commitments into concrete, measurable operational changes that generate immediate brand value and customer loyalty benefits. The awards program's expansion and recognition across multiple editions indicates that hospitality operators now perceive sustainability not as a compliance cost or reputational hedge, but as a direct revenue lever that attracts higher-spending, lower-churn customer segments and justifies premium pricing. For hospitality investors and operators, the Traveling for Happiness framework matters because it provides a standardized, third-party validated sustainability positioning that allows mid-market and independent properties to compete against international chains on values-alignment without requiring the capital intensity of net-zero infrastructure investments. The coming months will likely see increased operator participation in sustainability award programs and accelerated integration of sustainability narratives into marketing and distribution strategies, which will create a competitive dynamic where non-participating operators face increasing perception disadvantage among affluent, environmentally conscious travelers—particularly in European and North American source markets where sustainability values drive booking decisions for 35–50% of luxury leisure travelers.

The convergence of three distinct regional movements—Spring Hotels' Mediterranean consolidation signaling that European operators must achieve scale through acquisition, Thai AirAsia's secondary gateway expansion fragmenting Asian tourism distribution away from primary hubs, and TMG's sustained sales velocity validating Egypt's dual-track capital formation system—creates fundamentally different competitive dynamics across three critical hospitality markets through the coming months and into 2027. European operators face a consolidation imperative: standalone and small-chain properties will face simultaneous pressure from acquisition-focused competitors, international brand expansion, and distribution disadvantage unless they achieve scale through M&A or strategic partnerships before the window for favorable acquisition multiples closes. Asian operators face a distribution opportunity: properties positioned in secondary gateways (Hua Hin, Chiang Mai, secondary Thai islands) will benefit from improved air connectivity and reduced customer acquisition friction, while Bangkok-centric operators will face margin compression as carriers fragment capacity away from primary hubs. Egyptian operators and investors face a capital formation advantage: the combination of private developer momentum (TMG) and public market infrastructure (state IPO programs) creates a rare window where hospitality-linked real estate can attract institutional capital at lower cost of capital than competing emerging markets, rewarding developers and operators who can deploy capital into large-scale, multi-year projects before regional competition intensifies. The regional winners through 2027 will be European consolidators who achieve critical mass before acquisition multiples compress, Asian secondary-market operators who can capture the first wave of gateway-fragmentation demand, and Egyptian developers who deploy capital before the capital formation window narrows—while losers will be fragmented European independents, primary-hub Asian operators facing capacity cannibalization, and Egyptian operators who delay capital deployment waiting for improved macroeconomic conditions that may not materialize.

TMG Posts $4.5B In H1 2026 Sales On Record Second Quarter

Published 7d ago

Talaat Moustafa Group (TMG) reported first-half 2026 sales of $4.45 billion (EGP 219.1 billion), up 3.8% from $4.3 billion (EGP 211 billion) a year earlier, as record second-quarter performance and strong demand for key projects supported growth.TMG's H1 salesTMG said it generated $3.45 billion (EGP 170 billion) in sales during the second quarter, its strongest quarterly performance on record, up 27.8% compared with $2.7 billion (EGP 133 billion) in the same period of 2025, according to ...

OPEC+ Approves 188,000 Bpd Oil Output Increase For August

French Billionaire Bernard Arnault Hit With $25.7M Tax Assessment

A pilot explains why airlines have become so strict on luggage weight limits

Precious Metals Recover As Weak US Jobs Data Eases Rate Concerns

Published 8d ago

Precious metals recouped a portion of their recent losses during the first week of July after softer-than-expected US employment data lowered expectations for a Federal Reserve rate hike in September, ending a multi-week losing streak.The rebound, however, was insufficient to offset June’s sharp selloff, when all four major precious metals recorded significant monthly declines amid a stronger US dollar, higher Treasury yields, and expectations that US monetary policy would remain restrictive....

Six Qatari Companies Ranked In 2026 Forbes Global 2000

Clash Between Dallas Police, Egypt World Cup Team Members Goes Viral

Jordan Reclassified As Upper-Middle Income Economy By World Bank

UAE PMI Declines In June As Regional Conflict Weighs On Non-Oil Activity

Published 9d ago

S&P Global's UAE Purchasing Managers’ Index (PMI) fell from 52.6 in May to 50.8 in June, amid headwinds from the Middle East conflict, which continued to weigh on the domestic non-oil private sector. Non-oil private sectorThe seasonally adjusted PMI in June remained above the 50 baseline that separates economic growth from contraction. The UAE non-oil private sector experienced its weakest expansion in over five years during June, according to S&P Global on Friday. June’s challen...

US Labor Market Loses Steam As Job Growth Slows And Participation Drops

Precious Metals Rally As Weak US Jobs Data Fuels Fed Rate Expectations

48 ore alle Lofoten, le isole dei pescatori al di là della più convincente cartolina della Norvegia

Fondazione Don Gnocchi e Garden Toscana Resort: una vacanza che racconta il turismo accessibile

Published 10d ago

Il turismo accessibile non è un tema astratto. Per molte famiglie partire per un viaggio significa fare i conti con il budget, scegliere una meta, prenotare e preparare le valigie. Per altre, invece, ogni spostamento richiede un’organizzazione molto più complessa: ausili, farmaci, carrozzine, dispositivi medici, tempi di assistenza e tante cautele. Anche per questo, una L'articolo Fondazione Don Gnocchi e Garden Toscana Resort: una vacanza che racconta il turismo accessibile sembra essere il ...

Google Loses Final Appeal As EU Court Upholds $4.7B Android Antitrust Fine

Abu Dhabi's IHC, Adani Enterprises Sign MoU For $11.5B Aluminum Project In India

World Bank Approves $265M To Finance Ifahsa Pumped Hydropower Storage Project In Morocco

Tesla’s Electric Semi Has Its First Fatal Crash

Published 10d ago

Two people in a small Volkswagen Beetle died after the massive battery-powered truck slammed into them at a highway intersection in Nevada, not far from the factory that builds it.Tesla’s new electric Semi was involved in a crash earlier this week that killed two people, the first known fatal accident involving the carmaker’s newest model, which just went into regular production this year.According to reports from the Nevada Highway Patrol and Lyon County Sheriff’s Department, the 10-ton Tesl...

Cycling Scotland’s lost highways and byways: a two-wheel odyssey in the wilds of Sutherland

Sorrento, una piscina naturale mistica come il Parsifal di Wagner che qui litigò con l’amico Nietzsche

Saudi Arabia Draws $11B In Foreign Private Capital As Investor Base Expands Fivefold

Six of the best long-distance European trails to walk in summer

Published 12d ago

From a less-crowded camino and the Slovenian Alps to a stunning river trail and Ireland’s remote Beara peninsula Distance up to 74 milesDuration 3-9 days Continue reading...

5 Commercial Aircraft Programs Boeing And Airbus Cancelled

How A Single Test Flight Crash Set Back The B-52J Radar Program By Months

AirAsia checks potential for regional flights to Hua Hin

T+L leads relaunch of Phuket resort

Published 6d ago

PHUKET, 6 July 2026: Travel + Leisure Co. (NYSE:TNL) has relaunched the former Wyndham Sea Pearl Resort Phuket following a transformation and repositioning, unveiling a new identity as Club Wyndham Patong Hill Phuket. The resort debuts as a new premium offering and is the first Club Wyndham-branded resort in Thailand. The leading leisure travel company […] The post T+L leads relaunch of Phuket resort appeared first on TTR Weekly.

Air India serves up new cabins on London flights

SalamAir flies to Medan Indonesia

Ponant strengthens marketing team

MFTF’s second edition stands on a firm footing

Published 6d ago

KUALA LUMPUR, 6 July 2026: The Malaysian Association of Tour and Travel Agents (MATTA) hosted the 2nd edition of the MATTA Muslim Friendly Travel Fair (MFTF 2026) at the World Trade Centre Kuala Lumpur (WTC KL), 4 to 5 July. Visiting the event, YB Dato Sri Tiong King Sing, Minister of Tourism, Arts and Culture […] The post MFTF’s second edition stands on a firm footing appeared first on TTR Weekly.

La hoja de ruta de PortAventura World para integrar la sostenibilidad en la experiencia

Viajes Combinados: la respuesta a un viajero que quiere más en un solo viaje

Perú, un escenario MICE entre patrimonio, gastronomía y naturaleza

Spring Hotels activa una nueva etapa de crecimiento tras duplicar inventario

Así gana terreno Egipto en las agencias tras el frenazo de primavera

Premios Traveling for Happiness: pequeños cambios que generan grandes impactos

Not Done Yet: Breeze Airways Schedules Embraer E190 Flights On 9 Routes Over The Next 2 Months

This Airline's Premium Economy Has 4 More Inches Of Legroom Than Award-Winning Emirates & Qantas

Frontier Airlines To Shrink Its Fleet By Selling 11 Airbus A321neos To Avolon

TAG Says Tourism Tax Is Vital To Keep Fiji Connected To The World

Czechia Hotel & Chains Report 2026

AI Hospitality Alliance Survey Shows Demand for Practical AI Guidance and Standards

Denver airport to add underground passenger walkways between concourses

This Unknown Island Is The “Maldives” Of Croatia

Americans Can Now Fly Nonstop To Europe’s Safest Undiscovered Island Destination

These 5 Caribbean Islands Now Require All Travelers To Complete Digital Entry Permits

Renting an Airbnb this summer? Here are the best credit cards to use

Vanuatu launches first direct Christchurch flights as tourism recovery gains momentum

#PigOnBoard: Man Calls American Flight Attendant A Pig, Posts Her Picture Online (Shame On Him!)

Oltre Budapest: tre escursioni da non perdere tra lago Balaton, Szentendre ed Eger

Partner communications intensify as Singapore Cruise Centre takes new home

TUI Hotels abre un establecimiento en Fuengirola y firma un proyecto en Sevilla

El hotel como refugio urbano, nuevo concepto de la hospitalidad moderna

Hyatt Regency Barcelona Tower cumple 20 años como icono hotelero y referente MICE

These points hotels have turndown service worth traveling for

Airlines Are Turning Live Entertainment Into a Loyalty Strategy

Atmos Rewards Summit Visa card review: Stellar value for more than just Alaska Airlines and Hawaiian Airlines loyalists

Al via la prima verifica EPD per le mobile home del turismo open air

United Pilot Sues Marriott After Hotel Room Invaded By Bats, Leading To Bites, Rabies Shots

Forget Rome! Americans Can Fly Nonstop To 3 Of The Most Unique Cities In Italy Right Now

How to transfer credit card points to Hyatt

Croatia's lesser-known islands hide ancient villages, wild landscapes and crystal-clear seas

5 Of The Safest Caribbean Islands Worth The Splurge

United’s Cursed 787 Is Still “Broken,” Even After Being Sent Back To Boeing

VACAYA Plans First-Ever “Arabian Nights” Saudi Arabia Gay Cruise

Turkey Blocks Virgin Voyages Gay Cruise From Docking, Citing “Moral Standards”

Hospitality's real question isn't legal. It's cultural.

Turkey Refuses Entry to LGBTQ+ Cruise Carrying More Than 1,000 Americans

Calcio, ospitalità e identità locale: al Barbera il meetup degli host Airbnbo

Mincey Marble Manufacturing Sees Increased Demand as Hotel Conversion Projects Accelerate

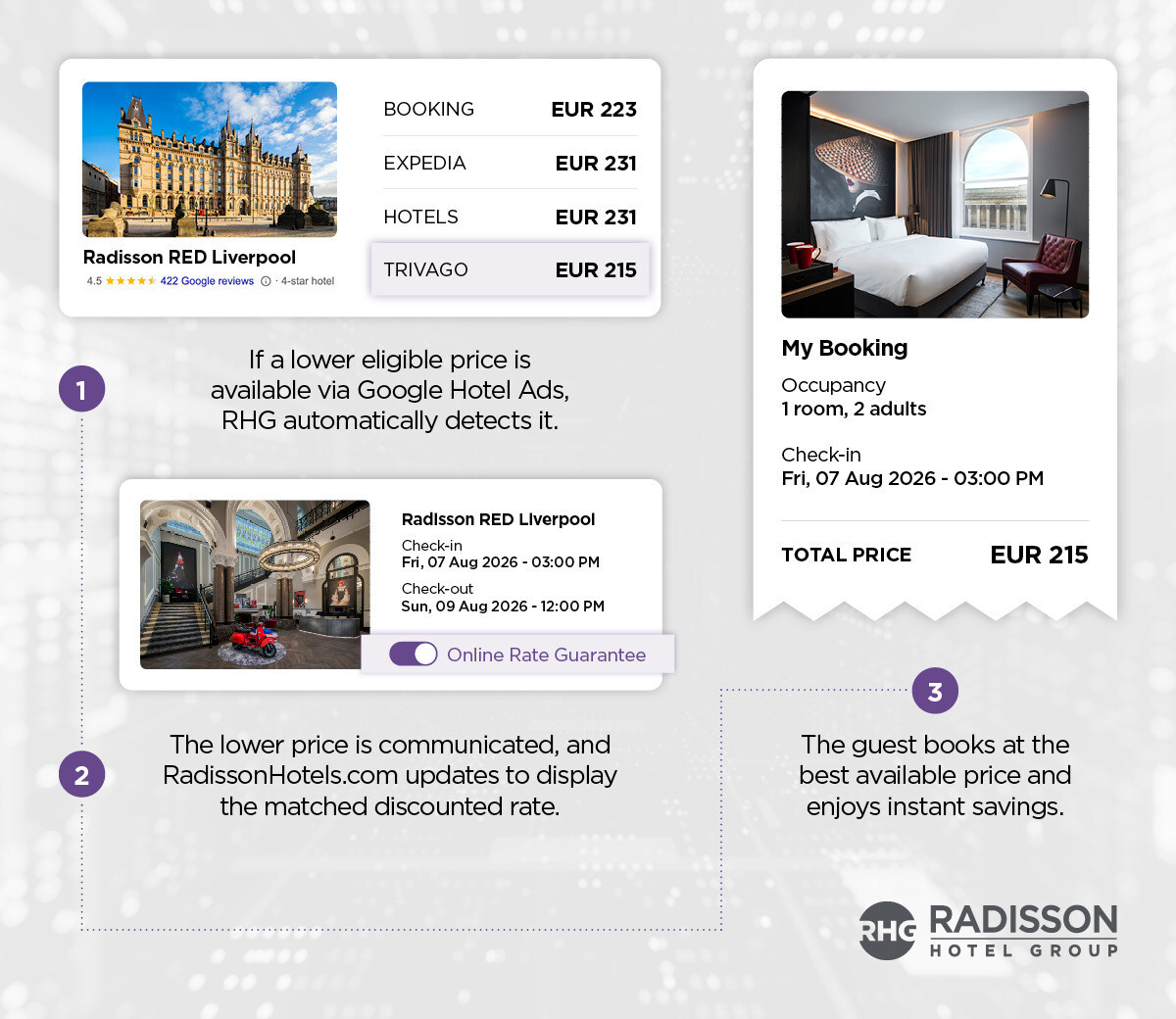

Radisson Hotel Group Launches AI-Powered Price Matching as Direct Booking Battle Enters a New Phase

Cabo Verde Made World Cup History — and Travelers Are Already Seeking It Out

Tarragona se hace cada vez más hueco en el mapa de cruceros del Mediterráneo

Las cadenas hoteleras lideran la rentabilidad del sector turístico en bolsa

La Asociación de Aerolíneas Regionales reivindica el papel de los vuelos de proximidad para la conectividad

El Grand Hotel Europa de Innsbruck recupera su esplendor como NH Collection

Ex-Saudia Boeing 777s in Iran Put Aviation Sanctions and Gulf Realignment in the Spotlight

The Dean Announces Opening of 281&Room Hotel in Munich’s Westend

Hotel Commercial Strategy Executives: Cautious Optimism, Uneven Reality

AI Progress in Europe Driven by Large Companies as Smaller Firms Lag

104&Room Hampton Inn & Suites Galveston Offered for Sale Amid Strong Market Performance

HOTREC is Hiring: Public Affairs Manager

The Amex Platinum's $200 airline fee credit is showing its age — here’s how I’d fix it

The biggest cruise ship ever built is about to debut in Europe

Why discipline is key to leveraging global opportunities

Unpublished Marriott Bonvoy Status Challenge For Gold & Platinum

The Harper Hotel appoints Andrew Oxley as general manager

Chase Sapphire Preferred Hotel Credit: Any Catch To This Easy $100 Benefit?

Marriott and Blacksand to develop 10 hotels across Saudi Arabia

AI Referral Traffic to Hotel Websites Surged 50%+, Fake AI Infographics Are Distorting Hotel Tech Decisions, U.S. RevPAR Climbed 9.6% on World Cup Demand

midarbast

August backs alkimii’s leading hospitality software platform

This Unknown Beach Town Is Puerto Rico’s Ultimate Hideaway With No Crowds

How an award-winning energy consultancy helps hotels mitigate energy costs

Naher Osten: Airlines starten wieder nach Tel Aviv

The Best Airbnbs in Sunny Malta, the Underrated Island Nation in the Mediterranean

Getting a refund for a canceled or delayed flight: What to know in 2026

Shiji's Natalie Kimball: hotels can't outspend OTAs on AI, but they can still win on experience

Hôtel de Paris Monte-Carlo: How Heritage Hotels Transform Place into Luxury Value

Tokyo, Paris and Athens lead US holiday travel demand for 4 July

Veratour fotografa l’estate: booking in ritardo, Italia regina

We need to talk about fake infographics

Wolves of Tokyo – a Japan Noir project by Run For The Hills

Aica e manageritalia sottoscrivono il rinnovo del Ccnl dei dirigenti alberghieri

-antler-raffia-hero-image-june-2026-pr.jpg)

Antler’s New Raffia Tote Bag Is the Ultimate Plane-to-Beach Chameleon

Air France Removes All Foreign Drinks In First & Business Class… Except One

American Airlines tornerà sulla Chicago-Tokyo dopo 7 anni, dal marzo 2027

Shore power is coming to Port of Québec's Cruise Terminal 30

The Marazion Hotel sold to first-time buyers

Five on Friday: July 3rd, 2026

Banor completes Hilton Garden Inn Silverstone restructuring deal

St. James’ Court completes major refurbishment

Goodwin opens retirement village with serviced apartments in Canberra

Best Airbnbs in Sardinia 2026

Hotel MOTTO appoints Daniela Kohoutek as general manager

Skopos Studio – new BOUTIQUE Design Schemes for 2026

Recent Hotel Technology Launches Show AI Moving From Standalone Tools Into Connected Hotel Operations

From volatility to resilience: redefining energy priorities for hotels

Minor Hotels cresce in Austria: acquisito lo storico Grand Hotel Europa di Innsbruck

United CEO Scott Kirby: United Is World’s Best Airline, USA Is World’s Best Country

The Most Luxurious Hotels and Suites on the Tour de France Route

9 of the best hotels in Naples for an authentic stay in the city

SeaSpace appoints Andrew Kitching as general manager

Open Air: estate incorona laghi del Nord, il Mezzogiorno tiene

Free hand luggage is coming to Europe thanks to new air passenger rights – here’s everything you need to know

Keeping an authentic voice when AI can’t read the room

The numbers behind AI's rise as a booking channel for independent hotels

Ethiopian Airlines attiva la rotta Addis Abeba-Lione

flyadeal launches first Italy services from Milan Bergamo

U.S. hotel results for week ending 27 June

Minor Hotels porta il brand NH per la prima volta in Medio Oriente

Eurazeo sells stake in Spain’s FST Hotels portfolio to Extendam

How Hilton Garden Inn Cancun Airport Uses Technology to Personalize the Guest Experience

AI-Powered Real-Time Price Matching Is Reshaping Travel — But Can It Really Guarantee the Best Deal?

Seychelles hosts 69th UN Tourism Commission for Africa

Kerten Hospitality rafforza la presenza in Kuwait con il nuovo Ray Hotel by Cloud 7

China Plans First Fully Robot-Operated Hotel Powered by AI and Robotics

Destination by Hyatt opens Parian Chronicle Hotel Paros

Atlas expands airline retailing platform

Harding+ adds Lucy Quartermaine jewellery to four ships

How AI-Powered Digital Mockups Could Reshape Hotel Design, Development and Procurement

Hotel Review: Trunk Hotel Yoyogi Park

TSA’s Crewmember Access Point (CMAP) Replaces Known Crewmember (KCM)

Brazil Sees Strong Rebound in German and European Tourism as Global Travel Demand Remains Resilient

Excellent Entertainment marks 25 years with Disney Cruise Line

Machine and Lionshead acquire 641-room Atlanta Airport Marriott

UK regulator launches battery safety campaign

Radisson rolls out AI-powered real-time hotel price matching

MarketHub Americas highlights regional travel growth

Cendyn wants hotels to get ahead of "OTA 2.0"

196+ forum Munich: Launch of the Hospitality UPGRADE Award 2026 – Spotlight on the Best Start-ups

Celestyal expands into the Western Mediterranean

Netflix's Amotti partners with Dream Cruises for fitness experience

How Young Leaders Connect, Grow, and Lead Through HSMAI Europe

Hotel Auronzo Dolomites entra in Meliá: 2 milioni di investimenti per il rilancio

Lago Maggiore: a Stresa debutta un nuovo hotel di lusso con spa private, rooftop e mostre d’arte

Turkish Airlines ripristina i collegamenti con il Medio Oriente

The Readiness Gap: Why Hospitality Graduates are Falling at The Final Hurdle

How mega events drive hotel demand and urban growth

How AI is helping hotels do more with less

Which airlines are flying to Dubai and Abu Dhabi? The latest flight updates

Sulle Dolomiti la nuova vita dell’Hotel Auronzo: diventa un Melià dopo il restiling da 2 mln

Nominations Open for the ISHC Lori Raleigh Award for Emerging Excellence in Hospitality Consulting

IHG Partners with Revolut on New UK Debit Cards Offering Elite Status and Bonus Points

15 brilliant summer pool day deals in Dubai

Regent Phu Quoc launches series of experiential residency programmes

Marriott debunks Gen Z myths in new luxury travel study

Japan’s tourism success lies in balancing tradition with flexibility

Greater Sentosa Master Plan to transform Singapore’s island getaway over two decades

Aviation roundup: Vietnam Airlines, Centrum Air and more

The Quiet Details That Shape a Hotel’s Spatial Identity

Emirates debuts next-generation lounge concept

Transforming vacations into experiences with Centara

Bartlett Unveils Jamaica’s Tourism 3.0 Framework, Calls for Caribbean ‘Co-petition’ at Americas Investment Forum

Crete and Ionian Islands Drive Growth as Greece’s Tourism Revenue Climbs

EOS Hospitality Names Ellen Kaplan Senior Vice President of Marketing

Whitbread Begins Construction of Premier Inn at Sandyford Business Park in Outer Dublin

Corinthia Hotels Names Peter Roth President of Hotel Operations

Fall Bookings, Arctic Adventures, and Private Villas Lead 2026 Luxury Travel Trends

Proud Island Nation Seychelles Hosts 69th UN Tourism Regional Commission for Africa

This New Charleston Hotel Is a Smart Choice for Women Travelers

IHG Hotels & Resorts Renews Partnership With Rugby Australia Through 2028

Call for 2026 BD Ones to Watch Nominations

Vow's Scanship firms €6.4m cruise newbuild order

Jamaica Urged to Invest in Sports Infrastructure to Unlock Tourism Growth

HUMAN TRAFFICKING PREVENTION

EU leaders call 'urgent meeting' with airlines as airport chaos grows

Marriott Outspends Rivals on TV, But Airbnb Owns the World Cup

Supersonic Passenger Travel Returns: FAA Rule Change Could Transform Air Travel

How Dog Haus’s new area director program could fast track growth, according to CEO

Marriott to open first branded apartment rental property in Cleveland

Chase Sapphire Preferred Bonus Hits 100K Points — Here’s What To Consider

Chase Sapphire Reserve Offering Marriott Bonvoy Gold Status Challenge

13 best places to visit in November 2026, according to the travel editors

Costas Livadaris lifts the lid on future-ready hospitality

The Hari Will Make Its Singapore Debut in 2027

Basel Talal on the power of a people-first approach in hospitality

IHG partners with Revolut and Visa for co-branded debit cards

NCLH, Port of Seattle commemorate Belltown maritime mural

Clavell takes COO role at Aman Group

Noble Investment Group’s Extended-Stay Bet Is Behind a 149-Hotel Buying Spree

ANNUA Signature opens Gran Hotel Margalida

Regent Seven Seas unveils Solara decks for Seven Seas Prestige

The best hotels in Saint-Tropez, from glossy spots to see and be seen to hillside retreats with an unexpected edge

Is Padel Replacing Golf as the Sport of Business?

Porta Rossa Hotel Firenze Colbert Collection reimagined by THDP

Turismo e finanza agevolata: al via il webinar sul nuovo Bando Green Tour 2026

Certares acquires Hyatt Regency Savannah in Georgia

Delta Pilots Subtly Blame Management For “Unacceptable” Flight Reliability

IHG launches EVEN Hotel and Staybridge Suites near Universal Orlando

Birth Tourism in the United States: History, Industry, Abuse & Trump’s Crackdown

Sweltering in NYC? 13 Hotel Pools to Jump In and Beat the Summer Heat

Calcot Manor and Spa opens luxury woodland treehouses

Are Doors On Business Class Seats A Big Deal, Or Just A Silly Gimmick?

Plane Crashing Into Beijing’s Tallest Tower Blamed On “Personal Reasons”

Hawaii Just Banned This Type Of Tourist Attraction

Three-in-one Asian dining coming to MSC World Asia

The Art of the Floor: how the right rug can transform a hotel interior

The Future of Luxury Travel Is Invitation Only

The 10 most beautiful outdoor hotel pools in the UK, that make Britain feel like a Mediterranean holiday

Avani Hotels & Resorts expands in Laos with new Vientiane hotel opening

Hawaiian Airlines’ New Oneworld Livery Signals a Changing Pacific Strategy

These are the snacks you need to protect your gut health when travelling, according to nutrition experts

Hotel101 to develop 770-room property in Bangkok

The Salthouse Hotel Unveils £5m Luxury Spa

Accor’s Swissôtel Residences to debut in Ras El Hekma

What attracts hotel investment today

Certares expands hotel portfolio with Hyatt Regency Savannah deal

The St. Regis Costa Mujeres Resort, Cancún – a refined enclave between land and sea

Rocco Forte “reinventa” Ulisse: un itinerario nella Sicilia del Mito per celebrare The Odyssey

Andrew Moore leads Rosewood Phnom Penh as MD

Booking.com Built Its India Business on Leisure — Now It’s Going Corporate

The Best Hotels Along the Cinque Terre, the More Laid-Back Alternative to the Amalfi Coast

Virgin Hotels Collection appoints CEO

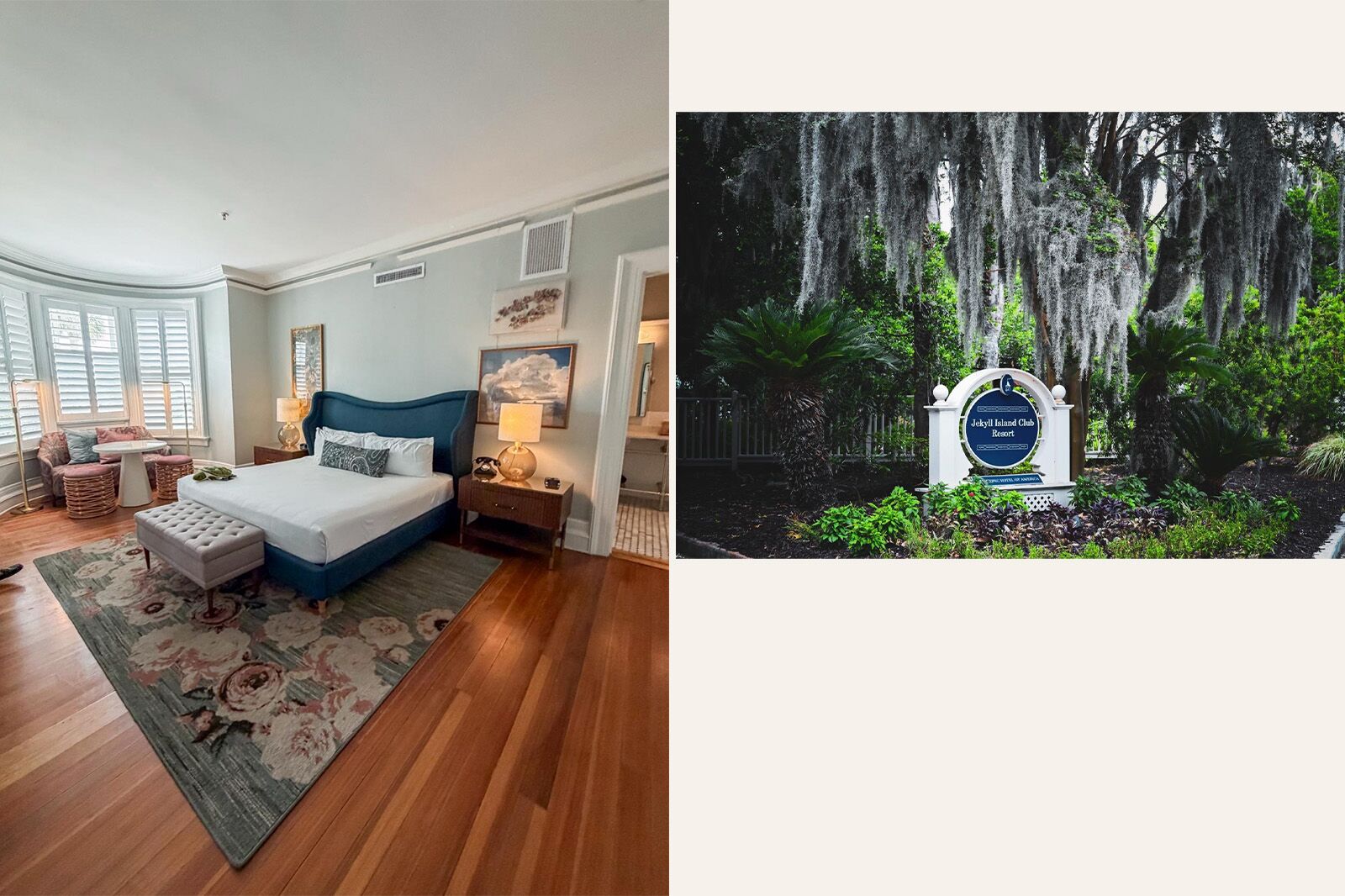

The Georgia Island Where the Rockefellers Wintered Is Now Public, and This Resort Has 3 Ways to Stay

Jamaica Hotel and Tourist Association (JHTA to Lead Jamaica’s Tourism 3.0 Growth Agenda, Says Bartlett

Seychelles Welcomes UN Tourism Leaders and African Delegates for Landmark 69th CAF Meeting

Antigua and Barbuda Art Week 2026 Opens Call for Artists and Creatives

Hotelier of the Year: Grupo Habita

This Denver Hotel Is Ahead of the Curve for Business Travel

Design Firm of the Year: Curioso

21 Best Charleston Airbnbs, From Colorful Cottages to Historic Homes

Expedia’s First IShowSpeed Video Brought Awareness. The Latest Pushes for Bookings.

Diageo World Class Lebanon 2026 celebrates bartending excellence with national finale

Beyond the standalone restaurant with chef Julien Guilloret of Jiwan

How AI is transforming the events industry

How AI-Powered Smart Thermostats Can Help Hotels Reduce Energy Waste and Improve Guest Comfort

Roads, Rails, and Rental Cars: Why the Future of Tourism Depends on Better Land Travel

The Hari Singapore set its sights on 2027

YOTEL’s Anti-Appy Hour Turns App-Blocking Technology Into a Hotel Wellness Experience

Six Senses Kanuhura Welcomes Global COASTS Project to Advance Seagrass Research in the Maldives

Top Six Travel Trends; the Fastest-Growing Traveler Segments

PPHE Hotel Group Partners With Hudini to Enhance Digital Guest Experiences Across European Hotels

IRIS Launches Guest Experience Revenue Calculator to Help Hotels Forecast F&B Revenue Uplift

Groupe GM Introduces Floral Street’s First-Ever Exclusive Hotel Line

Dal design al food&beverage, l’atmosfera di Milano definisce il nuovo volto dell’Hilton Milan

Top hospitality industry executive moves of Q2 2026

Hyatt Regency to bring first property to Tucson, Arizona

Flooring with character – why End Grain Oak is back in the conversation

‘From No New Zealand to New Zealand’ theme of NZCA conference

Upgrade every stay with TVs designed to make you money

Barceló Roma – a renovation inspired by Roman Rationalist architecture

Celestyal CCO Lee Haslett to leave for sports industry role

Alchemy 38 – a deep dive into holistic wellness design

Fred. Olsen's cruise-inspired music album drops

Fairmont is renovating 20 per cent of its global portfolio

Inside the factory: lighting the way with Mullan

RAD Hotel Group buys Lochgreen House Hotel & Spa

Restaurants Association Of Ireland Welcomes Permanent Return Of 9% VAT Rate

UK's Solent cruise capital worth £14.4b

Dar Global launches FENDI Casa villas at AIDA in Oman

Watkin Jones appointed to build Wilde aparthotel in Oxford

REIT acquires Jebel Ali Village townhouses in US $243mn deal

Mered introduces French Riviera-inspired villas on Al Reem Island

Hospitality Award, la Puglia regina dell’inclusione: il progetto dell’OOOM Homely Suites

2026 Readers' Choice Awards Survey

Inside the Rhode Island Resort With 3,500 Acres, Bentley Off-Roading, and Its Very Own Bourbon

.jpg)

11 Hotels Every Golf Lover Should Know About

From Reactive To Proactive: Leveraging Data To Prevent Device Failures & Protect The Guest Experience

These 10 Countries Have the Cleanest Beaches in the World

Inside London’s Art Hotel Built Around a Banksy Mural

Why the Bottom of the Funnel Should Come First in Hotel Direct Booking Strategy

Cruise Companies Are Finally Getting Strict About This Over-the-Top Behavior

Proposed legislation would help US ports battle drone threats

These Common Travel Scams Are Exploding Here’s How the FTC Says to Avoid Them

OneSpaWorld, Azamara announce major spa upgrades across fleet

WITT Expands Across Asia as Wellness Tourism Momentum Accelerates

WTTC Elevates Hotel Sustainability Basics to Independent Global Certification Scheme

Ambassador launches multi-decade entertainment cruise

Rotana targets 23 hotels in Saudi Arabia by 2027

Northern Lights makes British lighting more accessible

Jeddah Central Development Company bets on sports to drive growth reports CXO Ahmed AlAredhi

Hotel Tech-in: The dual-strategy loyalty product producing instant rewards

Capella Hotel Group appoints new Regional General Manager, Southeast Asia

Gunter Hotel in San Antonio joins Marriott’s Tribute Portfolio

The Tech Behind Optimization: AI in Hotels

One&Only launches sales for private homes in Fiji

The New Procurement Playbook: How Hotels Are Protecting Margins in 2026

Mandarin Oriental introduces its new resort – Mandarin Oriental Punta Negra, Mallorca

The Most Underrated Beaches in New Jersey

Prezzi: Confesercenti, si conferma fase resiliente economia. Pace ad Hormuz essenziale per rafforzare crescita

Dublin Hotels Effectively Full For Four In Every Ten Nights

Case study: Focus SB makes a statement at The Newman

Poltu Quatu, Marriott e Castello Sgr insieme per le W Residences: opening nel 2027

Think Twice Before Taking This Popular Vacation Photo in Alaska

Tao Group Takes Hospitality to New Heights at Hudson Yards

The Diplomat Channels Benjamin Franklin’s Legacy in Philadelphia

Taco Bell’s Cantina concept makes its airport debut

Emma Montgomery Design Makes Aubrey’s Corner Feel Like Home

BABEL Lille Hotel: a stopover on the Spice Route

Keep Your Outdoor Spaces Open for Business

Chambers Hotel New York reopens in Midtown as independent operation

Proposte: soluzioni di confine

Horizon Wellness & Spa Resort, relax en plein air

Forte dei Marmi, all’Hotel Principessa la bellezza inizia dall’ingresso

Nobu Brings Its Hospitality Concepts to Egypt

Paolimura Resort, Apartment & Spa: spazio alla luce

Habyt to open 319-unit Vienna aparthotel in August

The hotels AI recommends are not necessarily the best. They are the ones that showed up.

At Mine Hospitality adds two aparthotels in Miami Beach

News aggregated from leading international sources. Click any article to read the full story.